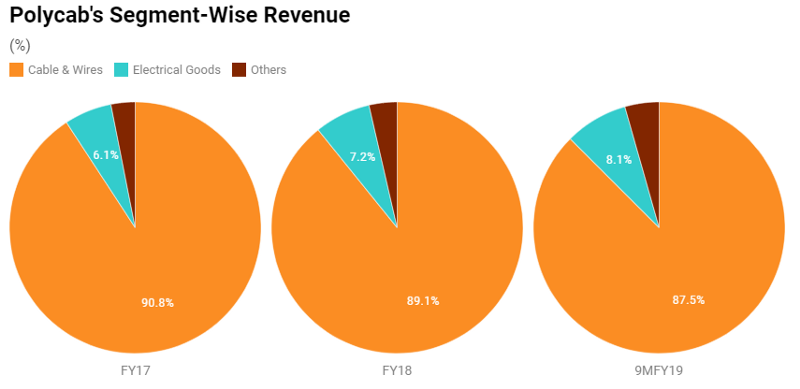

India’s largest manufacturer of electric wires and cables plans to raise nearly Rs 1,345 crore from its three-day initial public offering. Incorporated in 1996, Mumbai based Polycab India Limited is engaged in the business of manufacturing, selling and distributing wires, cables and Fast Moving Electrical Goods (FMEG) products. Some of the FMEG products produced by the company are solar products, luminaires, LED lighting, electric fans, and switchgear.

The company entered into an engineering, procurement and construction (“EPC”) business and FMEG business in 2009 and 2014, respectively. As on 31st March 2018, it has more than 3,300 authorized dealers and distributors, 100,000 retail outlets, 24 manufacturing facilities and 29 warehouses in India. All the sales and marketing activities of the company are handled through corporate.

Why Polycab is a good opportunity for the short term as well as for long term investors?

1. Strong financials:

Polycab’s revenue grew at an annualised rate of 11.1 percent in the four years through March 2018. The company’s net profit grew 42.7 percent in the same period. For the first nine months of the financial year 2018–19, the company reported revenue and a net profit of Rs 5,507 crore and Rs 358 crore, respectively. Earnings before interest, tax and depreciation and amortization grew at an annualised rate of 25.4 percent, while Ebitda margin averaged 9.2 percent in the four years through March 2018.

For the first nine months of the financial year 2018–19, the company reported an Ebitda and Ebitda margin of Rs 694 crore and 12.6 percent, respectively.

2. Debt to equity is .3

Polycab had a debt of close to Rs 620 crore as of Dec. 31, which would reduce to Rs 540 crore once the company uses part of the IPO proceeds to repay debt. The firm’s total debt-to-equity ratio is as low as 0.3 times, despite incurring a capital expenditure of over Rs 900 crore and distributing dividends at least in the last four years.

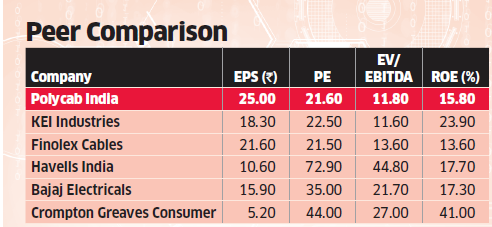

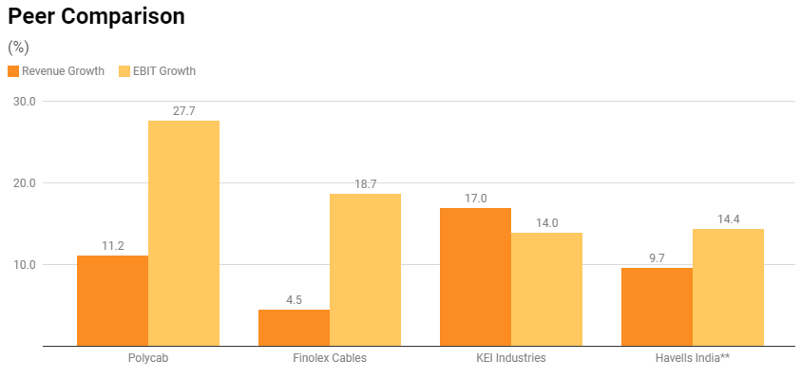

3. Peers And Valuations

Finolex Cables Ltd., KEI Industries Ltd. and Havells India Ltd. are Polycab’s nearest peers.

- Finolex Cables generates over 96 percent of its revenue from cables and wires.

- The corresponding figures for KEI Industries and Havells India are 75 percent and 32 percent, respectively.

- Havells India generates nearly half of its revenue making electrical goods.

- Polycab’s growth has been better than its peers in the four years through March 2018. For Havells India, we have considered the revenue and EBIT of its cables and electrical goods unit.

4. Dividend:

Despite incurring a capital expenditure of over Rs 900 crore and distributing dividends at least in the last four years.

5. Valuation:

Polycab’s earnings per share on an annualised basis for the financial year 2018–19, after the issue of new shares, would be close to Rs 32 and at the upper end of the price band, the price-to-earnings ratio stands at 16.7 times.

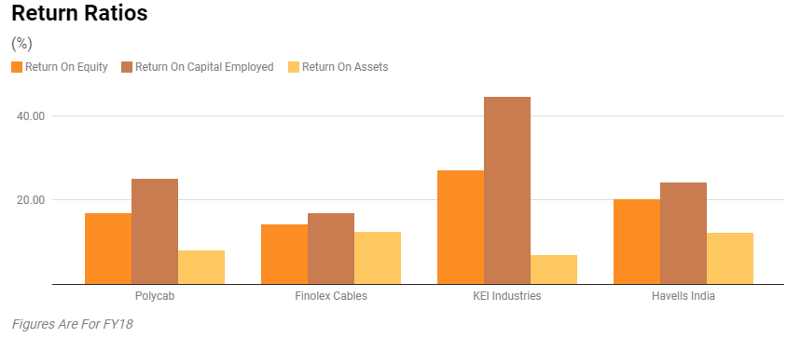

6. Return Ratios

Polycab’s return ratios have expanded in FY18 compared to the last year. Yet, it fails to match u with its peers on this count.

7. Future Strategies:

- Make market presence more prominent in wires and cables sector.

- Enhance and expand FMEG business.

- Increase reach by expanding the distribution network.

- Improve operational efficiency by investing in technology.

- Increase brand awareness.

8. competitive strengths

- Market leader in the respective segment in India.

- Diverse customer base.

- A range of electrical products.

- Established distribution network.

Issue Open Apr 5, 2019 — Apr 9, 2019

Face Value: Rs 10 Per Equity Share

Issue Price: Rs 533 — Rs 538 Per Equity Share

Employee Discount: 53

Market Lot: 27 Shares

Min Order Quantity: 27 Shares

Listing At: BSE, NSE

Hire a personal SEBI Registered advisor for your portfolio: Know moreLet the advisor design your Stock Portfolio for Long term:Know more